Unsecured credit

Introduction to unsecured credit

Unsecured credit refers to any credit product that doesn't require collateral backing from the borrower. Unlike secured credit, where lenders can repossess specific assets if borrowers default, unsecured credit relies entirely on the borrower's creditworthiness, income, and promise to repay.

Common unsecured credit products include traditional credit cards, personal loans, student loans, and most business financing. All else being equal, most borrowers prefer unsecured credit as financial difficulties would threaten their creditworthiness, but not their belongings. But creditors aren’t willing to extend unsecured credit in all cases, instead requiring borrowers to put up collateral.

Unsecured credit plays a central role in the modern lending landscape, representing the majority of consumer credit products. While secured credit serves specific niches like credit building or large purchases, unsecured credit handles the bulk of everyday consumer financing needs.

How unsecured credit products work and their market

Mechanics of unsecured credit

Unsecured credit operates on trust and statistical risk assessment rather than asset backing. Lenders evaluate applicants based on credit history, income stability, debt-to-income ratios, and other factors that predict repayment likelihood. Since there's no collateral to recover, lenders must be more selective about who they approve and more proactive about collections when accounts become delinquent.

The approval process typically involves automated underwriting systems. These systems pull credit reports, verify income through third-party data sources, and run applicant information through predictive models to deliver decisions in minutes.

Credit score requirements for unsecured credit

Most unsecured credit products target borrowers with good to excellent credit scores, typically 650 and above. This requirement exists because lenders need strong indicators of repayment ability when they can't rely on collateral for security. Borrowers with lower scores may still qualify for some unsecured products, but usually face higher interest rates, lower credit limits, or additional fees.

The credit score threshold varies significantly by product type and lender risk appetite. Premium rewards credit cards might require scores above 750, while some personal loan products accept scores as low as 580.

Application process and fraud prevention for unsecured credit

Since unsecured credit applications can be completed quickly online with minimal documentation, they're attractive targets for fraudsters. Lenders invest heavily in identity verification and behavioral analytics to detect suspicious applications while avoiding too much friction for legitimate applicants.

Modern fraud prevention combines automated screening with manual review processes. Machine learning models flag potentially fraudulent applications based on data patterns, while human investigators review flagged cases.

Interest rates and fees associated with unsecured credit

Unsecured credit typically carries higher interest rates than secured products to compensate for the additional risk. Credit card rates often range from 15% to 30% annually, while personal loans might range from 6% to 36% depending on the borrower's credit profile.

Fee structures vary widely but commonly include annual fees, late payment fees, overlimit fees, and foreign transaction fees for cards. Personal loans might include origination fees or prepayment penalties.

Evaluating unsecured credit products: Benefits and drawbacks

Pros of offering unsecured credit

Unsecured credit offers several compelling advantages for lenders. The streamlined application process allows for rapid scaling and lower operational costs since there's no need to evaluate, store, or monitor collateral. Borrowers appreciate that speed (as well as the lower liability for themselves), and customer acquisition tends to be easier as a consequence.

Revenue opportunities extend beyond interest income to include various service fees and cross-selling opportunities for other financial products. Card programs also introduce interchange fees paid by merchants.

Cons of offering unsecured credit

The primary challenge with unsecured credit is higher risk compared to secured products. Without collateral to recover, lenders face greater exposure when borrowers default. This risk requires more sophisticated underwriting, ongoing portfolio monitoring, and proactive collections strategies.

Economic sensitivity represents another significant drawback. During recessions, unsecured credit losses typically spike as borrowers prioritize secured debt payments to protect their homes and vehicles. Competition in unsecured markets is also intense, with established players offering attractive rewards programs that can be difficult for newer entrants to match.

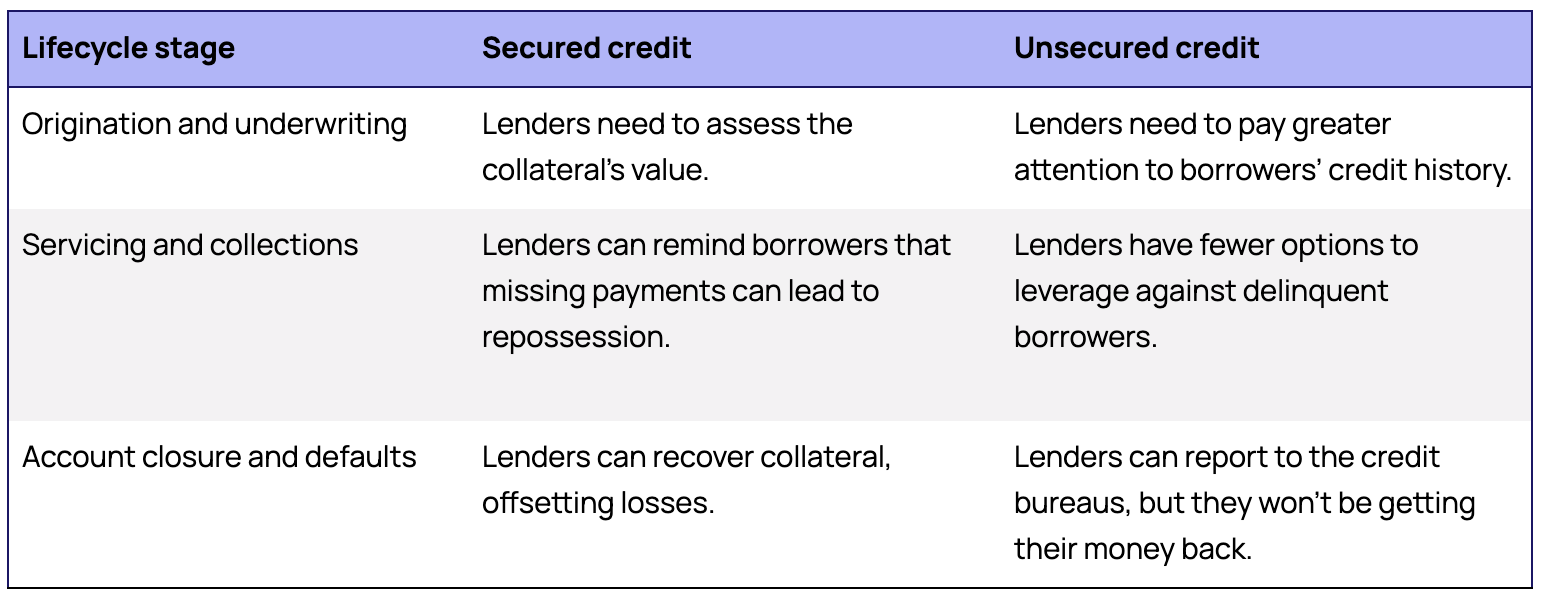

Comparison with secured credit products

Consider two near identical loans—same amount, interest rate, fees, and payment schedule—with the only difference being that one is an unsecured personal loan and the other is an auto loan, secured by a car. On paper, the loans look similar, but at every stage of the loan lifecycle, significant differences emerge.

Many successful lenders offer both product types, using secured credit as an entry point for newer borrowers and graduating them to unsecured products as their credit improves.

Building a responsible lending portfolio with unsecured credit

Strategies for successfully managing unsecured credit offerings

Successful unsecured lending requires sophisticated risk management and customer lifecycle approaches. Effective strategies include rigorous underwriting standards that balance approval rates with loss expectations, dynamic pricing models that adjust rates based on individual risk profiles, and proactive account management that identifies problems early.

Portfolio diversification across different customer segments, geographic regions, and product types helps manage concentration risk. Customer communication programs that educate borrowers about responsible credit use can improve payment performance while building loyalty.

Risk management and minimization techniques

Modern unsecured lenders employ multiple layers of risk management. Behavioral scoring models continuously assess account risk based on payment patterns and utilization changes. Early warning systems flag accounts showing signs of distress, enabling proactive intervention through hardship programs or modified payment arrangements.

Collection strategies for unsecured debt must be more creative since repossession isn't an option. Successful approaches include graduated contact strategies, payment plan options, and settlement programs for severely delinquent accounts.

Leveraging unsecured credit to build borrower credit

Responsible unsecured lending can help borrowers build credit while generating profits for lenders. Credit building features like automatic reporting to credit bureaus, credit score monitoring, and financial education resources add value for customers while encouraging responsible usage.

Some lenders offer graduation programs that increase credit limits or improve terms as borrowers demonstrate good payment behavior, rewarding responsible customers while encouraging continued engagement.

Bottom line

Unsecured credit presents a major opportunity, but not without risk. While the streamlined operations and broad market appeal make these products attractive, the inherent risks require sophisticated management approaches that many traditional lending platforms struggle to support.

Success in unsecured lending depends heavily on having technology that can handle complex risk modeling, real-time decision making, and dynamic account management. Without these capabilities, lenders often find themselves either approving too many risky accounts or missing opportunities with qualified borrowers.

If you're considering expanding into unsecured credit or looking to improve existing unsecured portfolios, we'd be happy to discuss what's worked for other lenders in similar situations. Reach out anytime to share your unsecured credit goals—we're always interested in exchanging ideas about effective approaches based on what we've seen across different markets.