Secured credit

Understanding secured credit

Secured credit refers to any credit product backed by collateral that the lender can claim if the borrower defaults on their debt. This collateral reduces the risk for credit providers, allowing them to offer more favorable terms or extend credit to borrowers who might not qualify for unsecured products.

Common secured credit products include secured credit cards (backed by cash deposits), home equity lines of credit and mortgages (secured by real estate), auto loans (secured by the vehicle), and increasingly, products backed by intangible assets like stocks, bonds, or even cryptocurrency holdings. Each type requires different approaches to collateral valuation, monitoring, and potential recovery.

The markets for secured and unsecured credit serve different purposes and customer segments. Unsecured credit might be appealing to every applicant, but creditors aren’t willing to extend unsecured credit to borrowers with bad or thin credit histories. Secured credit often attracts borrowers building or rebuilding credit, or customers who need larger credit amounts than they might qualify for with unsecured products.

Secured credit products: Common features and benefits

How does a secured credit product work?

Secured credit products require borrowers to pledge an asset as collateral before receiving credit. For traditional secured loans like mortgages or auto loans, the purchased item itself serves as collateral. With secured credit cards, borrowers typically provide a cash deposit that becomes their credit limit. More sophisticated products might accept investment portfolios, real estate equity, or other valuable assets. Pawn shops will accept just about anything valuable, from jewelry to first edition comic books.

The collateral provides security for the lender while potentially offering borrowers better terms than they'd receive with unsecured credit. If borrowers default, lenders can recover their losses by claiming and liquidating the pledged assets, though this process varies significantly depending on the collateral type and local regulations.

Benefits of offering secured credit products

For lenders, secured credit products offer several compelling advantages. Potentially losing your property encourages borrowers to make payments on time, ultimately reducing credit losses and leading to more predictable portfolio performance. This reduced risk often allows credit providers to offer more competitive interest rates, expanding their addressable market and attracting rate-sensitive borrowers.

Secured products also enable lenders to serve credit-building customers who might not qualify for unsecured credit, creating opportunities for long-term relationship development. Many borrowers start with secured products and eventually transition to unsecured offerings as their credit improves, providing natural upselling opportunities.

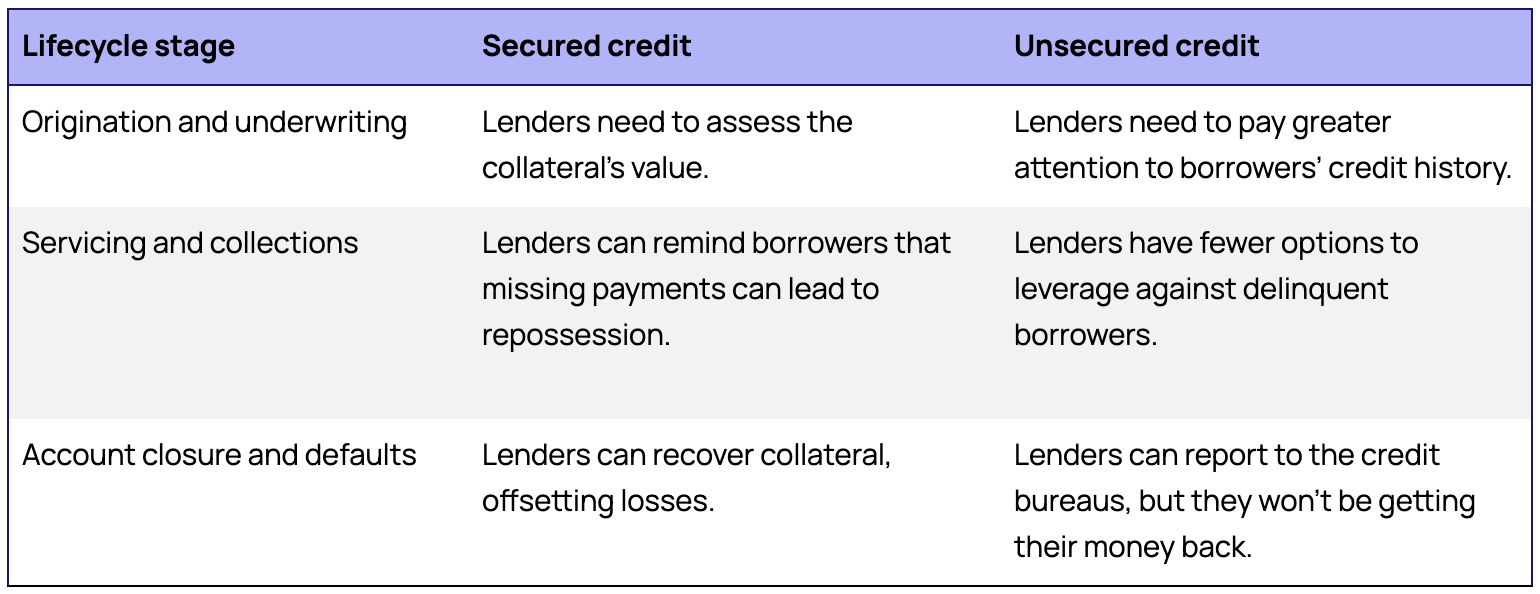

Differences between secured and unsecured products

The fundamental difference lies in risk allocation. Secured credit shifts default risk from the lender to the collateral, while unsecured credit relies entirely on the borrower's creditworthiness and willingness to repay. This distinction affects everything from underwriting criteria to interest rates to collections processes.

Additional differences emerge at different stages of the account lifecycle:

Secured credit for businesses

Business secured credit operates on similar principles but often involves more complex collateral arrangements. Commercial lenders might accept business assets like equipment, inventory, or accounts receivable as collateral. Some business credit products use personal assets from business owners as security, particularly for newer companies without substantial business assets.

Business secured credit can provide working capital, equipment financing, or general business expansion funding. The collateral requirements and evaluation processes tend to be more sophisticated than consumer products, often requiring professional appraisals and ongoing monitoring of asset values.

Implementing secured credit products

Managing different asset classes of collateral

Successful secured credit programs require robust systems for managing collateral. Traditional assets like real estate and vehicles have established valuation and recovery processes, but other asset classes present unique challenges.

Cash deposits are the simplest to manage—they're liquid, easily valued, and immediately accessible for recovery. Real estate requires professional appraisals, title searches, and foreclosure processes that vary by jurisdiction. Vehicles need ongoing monitoring for damage, mileage, and market value changes. Securities and cryptocurrency require real-time valuation tracking and specialized custody arrangements.

Each asset class demands different operational capabilities, from storage and insurance to valuation and liquidation expertise. Most lenders focus on specific collateral types to develop deep competency rather than trying to manage all possible asset classes.

Economic factors to consider when recovering collateral

Collateral recovery involves significant costs that can erode the benefits of secured lending. Repossession, storage, refurbishment, and sale expenses can quickly add up, particularly for lower-value items. Legal fees for foreclosure or repossession add further costs, and the time required for recovery means additional carrying costs for non-performing loans.

Market conditions heavily influence recovery values. During economic downturns, asset values often decline while the volume of collateral entering the market increases, creating unfavorable conditions for liquidation. Successful secured lenders build these economic realities into their underwriting models, ensuring that collateral values can absorb both recovery costs and potential market depreciation.

Ensuring a strong borrower experience

Despite the additional complexity, secured credit products must still deliver excellent customer experiences. From the outset, the credit provider can communicate clear expectations around collateral requirements, valuation processes, and potential recovery scenarios. Many borrowers appreciate understanding how their collateral affords them through lower rates and better terms.

During the application process, credit providers can minimize friction with tools to streamline submitting paperwork or gathering signatures, and use automated tools to underwrite borrowers and assess their collateral.

Transitioning customers from secured to unsecured products

While some credit providers only offer secured products, others offer them alongside unsecured options, often using secured credit as a stepping stone to unsecured products. As borrowers demonstrate responsible payment behavior and improve their credit profiles, they then become candidates for unsecured credit as part of a credit lifecycle journey.

Successful transition programs monitor customer payment performance, credit score improvements, and overall relationship profitability to identify upgrade candidates. What’s more, the relationship between the creditor and borrower might let them qualify for better rates as a repeat customer than they could if they switched to another provider. Done right, this transition is a win-win: it helps the borrower get greater access to credit and improves their overall experience, while at the same time earning reliable repeat business for the credit provider.

The bottom line

Secured credit products offer compelling opportunities for lenders to reduce risk while serving customers who need credit-building options or can’t get access to unsecured credit. However, managing collateral effectively requires specialized systems and expertise that many traditional lending platforms struggle to provide.

The complexity of tracking different asset types, managing valuations, and handling recovery processes demands technology designed specifically for secured lending operations. Without proper infrastructure, the administrative burden can quickly outweigh the risk reduction benefits that make secured credit attractive.

If you're considering launching secured credit products or looking to improve existing offerings, reach out to us. We'd love to discuss what's worked for other lenders managing similar collateral types.